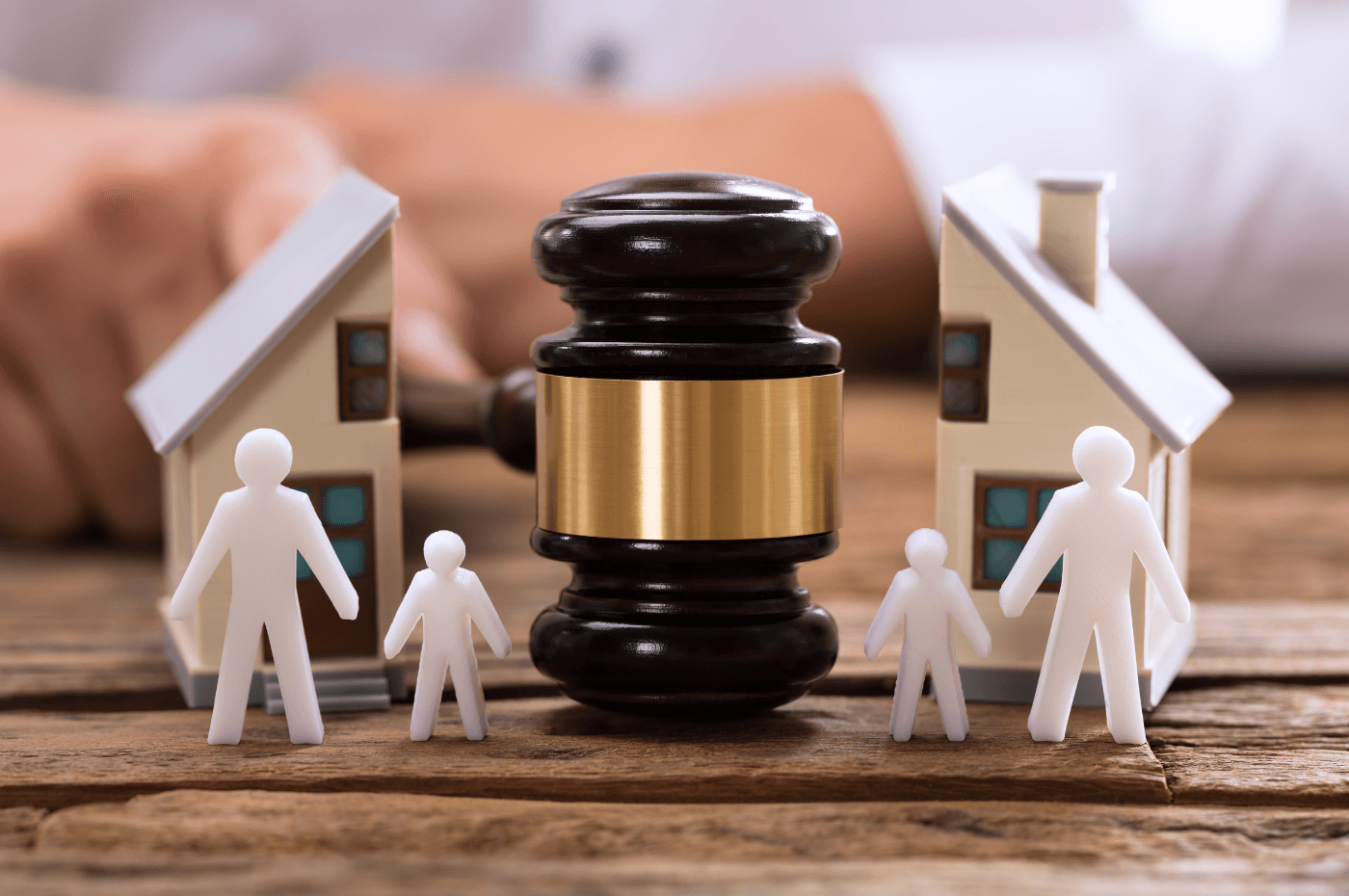

Separating from a spouse is already an emotional challenge. But when a house, a mortgage, and shared financial obligations are involved, the decisions quickly become more complex. Who gets the property? How should the value of the home be divided? And most importantly, what are the practical options available to help you move forward, without sacrificing your savings or your peace of mind?

In Quebec, whether you're married or in a common-law relationship, the rules governing the division of property after a separation vary significantly. It’s therefore essential to fully understand your rights, responsibilities, and the different avenues available: selling the home, buying out your partner’s share, or agreeing to take over the mortgage.

This article guides you through the main solutions available, based on your relationship status. It also offers practical advice to help you make an informed decision and avoid common pitfalls.

Quebec Law: how is property divided during a separation or divorce?

In Quebec, the rules for dividing assets after a separation depend on the couple’s legal status. Married couples are not governed by the same rules as those in common-law relationships. And since June 2025, a new legal category has been introduced: the parental union regime, which grants certain protections similar to marriage for common-law couples who have one or more children together. Let’s look at what each situation involves.

1. Separation or divorce for married couples

When two people are married, they are considered equal under the law, especially when it comes to dividing family property. This legal framework provides that, during a divorce, each spouse is entitled to half of the family assets accumulated during the marriage, which usually includes the primary residence.

In the case of a home, this means both spouses are legally entitled to 50% of the net value of the property, even if only one of them is listed as the official owner on the purchase agreement. In addition, the right to occupy the family home is protected: the non-owning spouse cannot be forced to leave the property unless ordered by a court.

2. Separation as common-law partners

Separation between common-law partners follows very different rules. In the absence of a legal marriage, there is no presumption of asset sharing, even after many years of cohabitation.

If the partners have signed a cohabitation agreement (also known as a domestic contract), this document will serve as the basis for determining how assets, including the home, will be divided.

If no such contract exists and only one of the partners is listed as the property owner, that person generally retains full ownership. However, they may choose, at their discretion and in accordance with the law, to allow the other partner to remain or to ask them to leave the home.

When both partners are co-owners, meaning both names are on the deed, they have equal rights to the property. Neither can force the other to leave without a mutual agreement or a court decision.

3. Separation under the parental union regime

Since June 2025, the parental union regime has introduced a new legal framework for unmarried couples who have at least one child together and meet certain conditions, including a minimum period of cohabitation.

This regime was created to better protect children and vulnerable partners. It grants certain patrimonial rights to these common-law couples, especially when a dispute arises during a separation. While this type of union does not provide all the protections of a legal marriage, it includes:

-

A fair division of certain assets, including the primary residence, according to specific rules defined by law;

-

The right to remain in the home for the parent with primary custody of the child, in certain cases;

-

The ability for a judge to rule on the division of the property, even if only one partner is listed as the owner, when fairness criteria are met.

This regime is not automatically applied. You must verify whether your situation meets the legal criteria, and if necessary, request official recognition of the regime. A notary or lawyer can assist you with this process.

Keeping or leaving the home: how to separate when you co-own a property

When a couple separates, one fundamental question arises: what should be done with the family home? This property, often the most significant both financially and emotionally, cannot always be kept by both parties. It is therefore crucial to understand the different options available.

Generally, couples, whether married, in a common-law relationship, or under the parental union regime, have three main choices:

-

Sell the property and divide the proceeds;

-

Buy out the other partner’s share to become the sole owner;

-

Sign a mortgage assumption agreement.

Before making such an important decision, it is strongly recommended to consult a notary or a family law professional. Their expertise can help avoid costly mistakes, clarify the legal implications of each option, and ensure the agreement complies with current legal requirements.

1. Selling the family home and dividing the proceeds

This is often the simplest option to consider, especially when neither party wishes to keep the home. It provides a clean break, both financially and emotionally. Selling ends the co-ownership and allows both parties to start fresh.

-

For married couples, the profits from the sale are typically split equally, in accordance with family property laws.

-

For common-law co-owners, the division depends on any agreements made or on the ownership percentages indicated in the deed (for exemple, 50/50 or 60/40).

-

Under the parental union regime, specific rules may apply if the home is considered a protected asset or if one parent retains use of it to ensure the child’s stability. Legal advice is highly recommended in such cases.

To maximize your property’s value and ensure a smooth process, work with a real estate broker. This professional can guide you through the steps of the sale, help set a fair price, and reduce potential conflict between ex-partners.

2. Buying out your partner to become the sole owner

If one of the partners involved in the divorce or separation does not wish to sell the property, it is possible to transfer the mortgage to just one of them. As with a sale, it’s important to first check with your financial institution whether a penalty will apply for breaking your mortgage contract, if it has not yet reached its term.

Next, you’ll need to determine the current market value of your property. To obtain an accurate assessment, it is recommended to hire a certified appraiser who can determine the fair value of the home based on market conditions.

How to calculate the buyout amount during a separation

The financial compensation required to buy out your partner’s share will be based on the following calculation:

Property value – remaining mortgage balance – penalty fees = net equity

Net equity ÷ 2 (or according to ownership shares) = amount payable to the partner for their share

Example:

Your home is worth $500,000. You co-own the property equally with your ex-partner. At the time of the transaction, $315,000 remains on the mortgage. Your lender also charges a $4,500 penalty for breaking the mortgage contract.

$500,000 – $315,000 – $4,500 = $180,500

$180,500 ÷ 2 = $90,250

To buy out your ex-partner’s share and become the sole owner, you would therefore need to pay them $90,250.

How do I know if I qualify financially to keep the house after a separation?

Before the transfer can take place, the partner wishing to keep the property must prove they are financially able to take over the mortgage alone. This means demonstrating sufficient income, a good credit score, and that the mortgage payments are up to date.

If the partner cannot qualify on their own, it is possible to bring in a co-borrower (or guarantor) who agrees to be legally responsible for the loan. The co-borrower must also demonstrate the financial capacity to repay. Before entering such an agreement, it is strongly advised to fully understand the responsibilities involved, as the co-borrower becomes legally bound to repay the mortgage in the event of default.

3. Signing a mortgage assumption agreement

When one partner agrees to take over the mortgage solely in their name, the co-owners may sign a mortgage assumption agreement. This arrangement allows one of the former partners to remain in the home and take full responsibility for all mortgage payments.

This type of agreement is usually considered a last resort, used when selling the property would result in a loss, or when the penalties for breaking the mortgage are too high. It also avoids the need to negotiate a brand-new mortgage.

However, it's important to understand that a mortgage assumption agreement does not automatically remove the departing partner’s name from the mortgage. As long as the debt is not fully transferred or renegotiated, both partners remain legally responsible for the loan, even if only one is making the payments. This can have significant consequences, especially for the non-occupying partner’s ability to take on a new mortgage or obtain other credit.

Do you need to sell your home because of a separation?

XpertSource.com can help you find a . When you tell us about your project, we put you in touch with qualified resources for free. Simply fill out our form (it only takes a few minutes) and we will connect you with professionals.