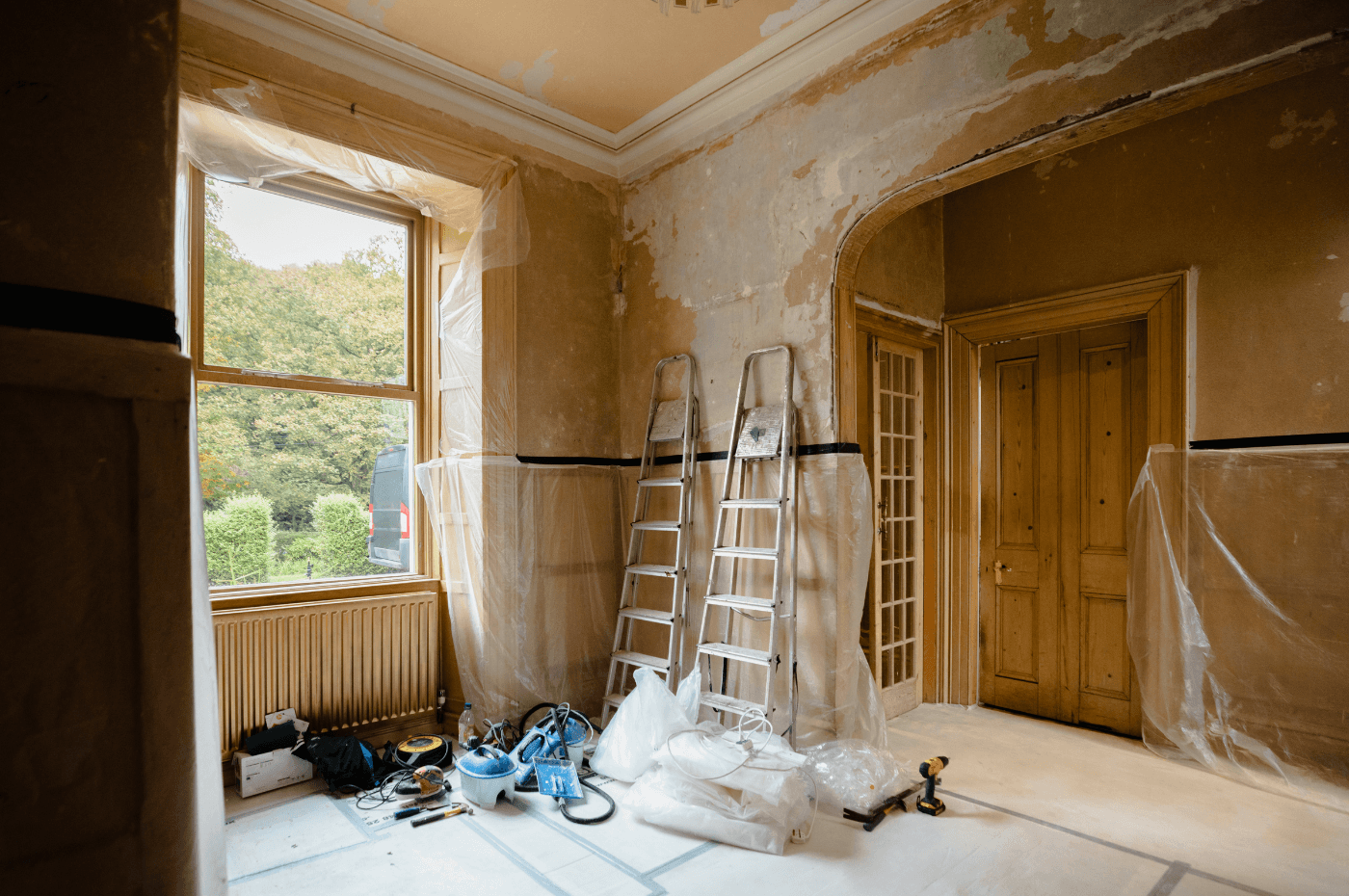

You’ve found the house of your dream... almost. There’s just one thing missing. Have you always envisioned living in a home with an open-plan kitchen and living room? While the house you love may need some work, you can easily see its full potential after renovations.

However, not all new homeowners can afford to renovate when purchasing a property. Some may even choose a home that requires less investment instead of the one they truly desire.

Whether you’re planning aesthetic updates or structural improvements, a purchase-renovation mortgage loan could be the ideal solution.

Here’s everything you need to know about it.

What is a purchase-renovation mortgage loan?

A purchase-renovation mortgage loan, also known as a renovation mortgage, is a type of loan that combines the cost of purchasing a property with the expenses for renovations. This loan is an excellent option for potential homeowners who may not otherwise be able to afford both buying and renovating a home at the same time, allowing them to invest in properties they might not have considered otherwise.

Can the loan be used for any type of work?

No, the renovation funded by a purchase-renovation mortgage loan must be permanent. You can make updates like installing new floors, replacing the roof, or renovating the kitchen. However, the loan cannot be used to purchase appliances or furniture for your home.

What are the eligibility requirements?

To qualify for a purchase-renovation mortgage loan, you must:

-

Be eligible for a mortgage loan insurance.

-

Have a minimum credit score of 600.

-

Purchase a home with a price of less than $1,000,000.

To apply for the loan, you must provide a work estimate to your lender. This estimate helps the lender determine your eligibility and the loan amount you may qualify for.

How is the loan disbursed?

Typically, the lender will approve up to 20% of the home’s purchase price or up to $40,000, whichever is lower.

The full loan amount is not usually given upfront. Here’s how it typically works:

-

Part of the loan is provided when you purchase the home.

-

The remaining funds are given once the renovation work is completed.

In some cases, if the renovation costs are less than 10% of the home’s purchase price, you may receive the full loan amount at once. If the renovation costs exceed 10%, the loan may be disbursed in instalments (up to four payments).

What happens if you change your renovation plans?

You must stick to the renovations that were approved by your lender. If you alter your project, you could lose eligibility for the loan. In that case, you may have to pay for the changes yourself or cover any additional costs.

How is the work verified?

An appraiser from the lender will inspect the renovations to make sure they were done according to plan. If the renovation costs are under $10,000, most lenders will just ask for invoices as proof of the work.

What’s the required down payment for a purchase-renovation mortgage loan?

The down payment for a purchase-renovation mortgage loan can vary depending on factors such as your financial situation, the type of property, and its purchase price. Here’s a general breakdown:

-

For 1 or 2-unit properties, the down payment if 5% if the purchase price is under $500,000, and typically 10% or more if the price exceeds $500,000.

-

For 3 or 4-unit properties, a 10% down payment is required.

-

For small rental properties, the required down payment is 20%.

As noted earlier, most lenders will set the renovation loan at 20% of the home’s purchase price, up to a maximum of $40,000. However, if you make a down payment greater than 20%, you could be eligible for a renovation loan of up to $60,000.

Renovation at purchase: what are other options?

The purchase-renovation mortgage loan offers several advantages for homeowners looking to renovate their new home right after purchase. Since the renovation costs are added to your mortgage, repayment is spread over a longer period, typically 25 years, which is the same as your mortgage’s amortization period. Additionally, the interest rate on the renovation portion is the same as your mortgage rate, which is usually more favourable than taking out a separate loan.

However, depending on your specific needs, the renovation cost, and your eligibility for this loan, other financing options might also be worth considering. These alternatives include:

-

Using your saving.

-

Refinancing your mortgage.

-

Applying for a home equity line of credit.

-

Applying for a personal line of credit.

-

Applying for a personal loan.

-

Using your credit card.

Are you looking to secure a mortgage loan?

XpertSource.com can help you in your efforts to . By telling us about your project, we will refer you to top-rated experts, free of charge! Simply fill out the form (it only takes 2 minutes) and you will be put in contact with the right experts.